Maintain Extra of Your Cash

[ad_1]

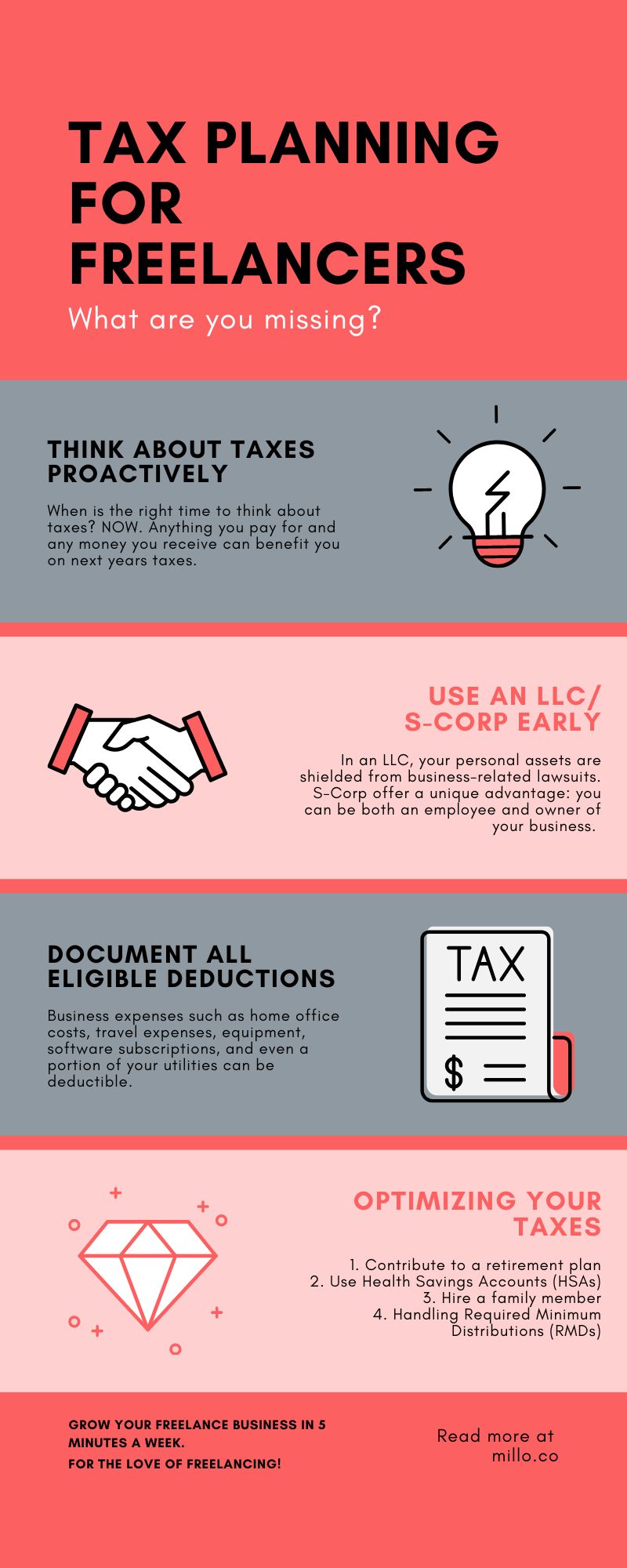

- When you don’t beginning fascinated about taxes till January you’re already behind. Planning now saves time for you later.

- Tax planning as a freelancer solely appears daunting till you begin doing it. It’s straightforward to procrastinate, however when you begin tax planning, life turns into simpler and sooner or later.

- Don’t overlook deductions! That is the commonest factor that freelancers fail to do, any expense associated to enterprise operations is tax deductible.

Failing to Assume About Taxes Proactively

Keep in mind, you’re primarily a small enterprise proprietor. Freelancers typically make the error of treating their taxes as an afterthought, solely contemplating them when tax season rolls round. This reactive strategy can result in missed alternatives for deductions and tax financial savings.

Proactive tax planning for freelancers, or anybody actually, entails common opinions of your earnings, bills, and potential deductions all year long. This ongoing course of lets you determine tax-saving alternatives, make mandatory changes, and keep away from undesirable surprises come tax season. It’s important to seek the advice of with a tax skilled who may also help information your selections and supply recommendation tailor-made to your particular state of affairs.

As a common rule of thumb, to guard your self, put aside 25-30% of your earnings for taxes. It will allow you to keep away from the dreaded ache of owing 1000’s of {dollars} come tax season.

Failing to Use an LLC/S-Corp Early

Many freelancers function as sole proprietors, unaware that altering their enterprise construction might supply important tax benefits. Working as an LLC (Restricted Legal responsibility Firm) or S-Corp can present authorized safety and tax advantages.

In an LLC, your private property are shielded from business-related lawsuits. On the tax facet, an LLC offers flexibility as earnings and losses can go by means of on to your private earnings with out going through company taxes.

S-Corps, however, supply a singular benefit: you may be each an worker and proprietor of your corporation. This lets you pay your self a “affordable wage” and take extra earnings as distributions, which aren’t topic to self-employment tax, probably saving you 1000’s every year.

Failing to Doc All Eligible Deductions

Freelancers typically overlook beneficial deductions. Enterprise bills comparable to dwelling workplace prices, journey bills, gear, software program subscriptions, and even a portion of your utilities may be deductible. It’s essential to maintain detailed data of all of your business-related bills all year long.

Keep in mind, correct documentation is vital. The IRS requires proof of all bills claimed as deductions. So, save your receipts, invoices, and financial institution statements. Think about using a cellular app or cloud-based system to trace your bills and retailer your data digitally.

Optimizing Your Taxes

Tax optimization entails utilizing authorized methods to scale back your tax legal responsibility. Listed below are some tax planning methods freelancers can take into account:

1. Contribute to a retirement plan: Self-employed people can contribute to a Simplified Worker Pension (SEP) IRA or a Solo 401(ok) plan. These contributions are tax-deductible, and the funds develop tax-free till retirement.

2. Leverage Well being Financial savings Accounts (HSAs): When you’ve got a high-deductible well being plan, you possibly can contribute to an HSA. Contributions are tax-deductible, and withdrawals for eligible healthcare bills are tax-free.

3. Rent a member of the family: When you’ve got kids or different dependents, take into account hiring them. You possibly can deduct their wages as a enterprise expense, and so they could also be in a decrease tax bracket.

4. Dealing with Required Minimal Distributions (RMDs)

When you’ve contributed to retirement accounts like a 401(ok) or an IRA, you’ll have to start out taking RMDs once you attain the age of 72. RMDs are calculated based mostly in your life expectancy and account balances. Failing to take your RMD may end up in a hefty penalty—50% of the quantity you need to have withdrawn.

In planning for RMDs, take into account the next methods:

- Think about a Roth Conversion: In case your conventional IRA or 401(ok) funds are transformed to a Roth IRA, you possibly can keep away from RMDs, as Roth IRAs do not need this requirement. Nonetheless, do not forget that you’ll owe taxes on the quantity transformed.

- Certified Charitable Distributions (QCDs): In case you are charitably inclined, you may make a QCD out of your IRA. This distribution goes on to the charity of your alternative, counts in the direction of your RMD, and isn’t included in your taxable earnings.

- Strategic Withdrawals: When you retire earlier than the RMD age, take into account withdrawing out of your retirement accounts strategically to attenuate the affect of RMDs in your tax bracket later.

You Work Onerous For Your Cash, Maintain It

Navigating the tax panorama as a freelancer may be difficult, however proactive tax planning may also help you reduce your tax legal responsibility and maximize your earnings. Frequently reviewing your earnings and bills, working underneath the proper enterprise construction, precisely documenting deductions, optimizing your taxes, and planning for RMDs are all key methods.

All the time seek the advice of with a tax skilled to make sure you’re making the perfect selections on your distinctive state of affairs. Proactive tax planning isn’t just about saving cash—it’s about constructing a stable monetary future.

Turn into much more monetary sound through the use of our free Freelance Fee Calculator.

Maintain the dialog going…

Over 10,000 of us are having day by day conversations over in our free Fb group and we might like to see you there. Be a part of us!

[ad_2]

You may also like

25 Forms of Pages that Each Blogger Ought to Contemplate

The Simple Means To Pace Up WordPress